According to the Western Fire Chiefs Association, in the United States, wildfires now burn nearly twice as much tree cover as they did in 2004, with an additional three million hectares of tree cover lost every year.

And as wildfires have worsened, they’ve evolved beyond the status of seasonal natural disasters: they’re now year-round crises that increasingly involve worsening climate conditions, insurance challenges, and homeowner uncertainty.

In this study, we’ll take a deep dive into America’s wildfire crisis to uncover all the key data. Let’s start by looking closely at a U.S. disaster that, for many, perfectly symbolises a growing national crisis.

The 2025 Los Angeles Wildfires

On January 7, 2025, the Palisades and Eaton Fires ignited just hours apart. They quickly turned into two of the most devastating wildfires in California history.

The Palisades Fire was belatedly initiated by the smoldering Lachman Fire, which was first suppressed on January 2, but which reignited six days later under extreme Santa Ana winds and dry conditions.

Over 8,000 firefighters spent 24 days containing the fires. Ultimately, the fires:

- Killed 31 people

- Destroyed more than 16,000 buildings, including around 12,000 homes

- Burned around 23,000 acres

- Devastated communities such as Pacific Palisades, Topanga, Malibu, and areas around Pasadena.

The combined economic losses are estimated at between $76 billion and $131 billion, with insured losses projected between $40 billion and $45 billion, making the January 2025 Los Angeles fires the costliest wildfire event on U.S. record. Total economic damage has been estimated as high as $275 billion, which eclipses previous record-setting disasters such as California’s 2018 Camp Fire and the 2023 Maui wildfire.

Call or text (800) 900-0000 or complete a Free Case Evaluation form

Wildfire Trends Across the United States

And wildfire activity continues to intensify across America.

In 2025 alone:

- 77,850 wildfires burned over 5.1 million acres

- Fire totals surpassed both the five- and ten-year averages

- 18,385 buildings were destroyed, including 12,773 homes

- Southern California accounted for 16,324 of those destroyed buildings.

Lightning caused around 8,300 of the fires (burning more than 2.6 million acres), while fires caused by humans continued to represent the majority of wildfire ignitions across the United States.

As of June 23, 2026:

- 34,262 wildfires have burned over 2.7 million acres

- 31 large fires are being actively suppressed

- Nearly 5,900 workers have been assigned to repel fire activity in the U.S., and

- Fire activity is largely concentrated across the Great Basin, Southwest, Northwest, and in Alaska.

Yet, in terms of geographical fire concentration, the situation is evolving.

Call or text (800) 900-0000 or complete a Free Case Evaluation form

Expanding Geographic Risk

Until relatively recently, U.S. wildfire risk was largely limited to the western United States. But this is rapidly changing. During 2026, the Morrill Fire became the largest in Nebraska’s recorded history. Additionally, two major wildfires in southern Georgia burned over 50,000 acres and destroyed over 120 homes, representing the state’s most destructive recorded wildfire.

Such events reflect not only an expanding geographical fire zone but increasingly extended wildfire seasons, with dangerous fire conditions now lasting from late spring into autumn.

The growing frequency, danger level, and geographic spread of wildfires clearly confirm the extent to which they now represent a national challenge. And it’s one that demands year-round preparation, higher levels of fire-repellent intervention, and growing investment in wildfire prevention.

One key reason that modern fires are so hard to extinguish is the ‘zombie’ factor.

Call or text (800) 900-0000 or complete a Free Case Evaluation form

‘Zombie’ Fires and Secondary Environmental Ignitions

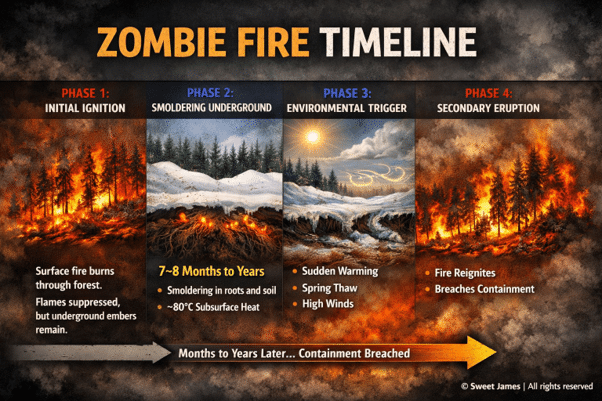

‘Zombie fires’ (also known as holdover or overwintering fires) are wildfires that seem on the surface to have been extinguished. Yet zombie fires continue to smolder in peat, roots, or organic soils before reigniting months (or even years) later when conditions become more fire-favorable.

Recent peer-reviewed research makes it clear that zombie fires can survive for 7-8 months under layers of snow and frozen ground, and then re-emerge during spring when the soil dries. New modeling studies reveal that peat soils can retain smoldering temperatures right through winter via retained and microbe-generated heat, meaning there’s an enduring, unseen underground source of ignition.

2025 field studies found that some zombie fires were remnants from wildfires many years earlier (including sites dating back to 2009), with many sites capable of repeated reignition.

A number of environmental conditions help to create zombie sites that can reignite.

- Peat and organic soils that quickly dry after snowmelt

- Increased exposure to oxygen as frozen ground thaws

- Rapid warming that reactivates underground fires

- High winds that exacerbate combustion and spread embers.

Although hundreds of zombie fires have consistently blighted Canada’s boreal forests, they’re relatively rare in the United States. Yet warming U.S. temperatures have increased both their frequency and severity.

Satellite data identified 20 major zombie fires across Alaska and Canada’s Northwest Territories between 2002 and 2018, with researchers making a clear link between frequency and severity and the hottest summers on record.

California has experienced two of America’s most significant documented zombie fires.

- 1991’s Tunnel Fire near Oakland, which reignited under dry, windy conditions, killed 25 people and destroyed nearly 3,500 homes.

- 2025’s Palisades Fire (2025).

Investigators believe the Palisades Fire’s zombie origins were due to Jonathan Rinderknecht, 29, who allegedly started the original Lachman Fire using a barbecue-style lighter on January 1, 2025. Prosecutors allege the fire smoldered underground before reigniting as the Palisades Fire on January 7.

Rinderknecht has pleaded not guilty to federal charges, including arson and destruction of property by fire. If convicted, he faces up to 45 years in prison.

These events show that wildfires often spiral out of control and cannot necessarily be contained. Under the right mix of environmental conditions, zombie fires can smolder and wreak havoc again and again.

Call or text (800) 900-0000 or complete a Free Case Evaluation form

Declining Real Estate Values and Long-Term Displacement

The 2025 Los Angeles wildfires caused massive amounts of damage and long-term displacement across the Pacific Palisades and Altadena. Around 40% of one-family homes were damaged, with an estimated 100,000 residents forced to flee.

Nine months after the fires, 70% of those who lost their homes were still displaced. A Department of Angels survey found that 90% of Pacific Palisades residents and 80% of Altadena residents were still without a home.

Property Value Losses

The wildfires effectively erased an estimated $8.3 billion in residential property value across the two communities.

- The value of destroyed homes dropped from $14.7 billion to $10.8 billion.

- The value of fire-damaged homes that are still standing fell from $2.2 billion to $1.9 billion.

- Undamaged homes from within the burn zones were not exempt from this trend. Their collective value declined from $10.4 billion to $9.4 billion in Pacific Palisades and from $3.8 billion to $3.2 billion in Altadena.

On average, homes destroyed by the fires and later sold as vacant lots sold for half their pre-fire purchase values.

Slow Reconstruction

The rebuilding of destroyed homes has not met demand.

- In Pacific Palisades, over 1,400 rebuilding permits have been issued, over 1,700 plans approved, and the construction of over 400 homes has begun; despite this, only two homes have been built.

- Altadena has issued more than 1,100 permits, but only four single-family homes have been built, one large, multi-family property, and three accessory dwelling units.

- In Malibu, where nearly 600 homes were destroyed, just 22 rebuilding permits have been issued.

Because of a combination of rising construction costs, permit delays, and limited housing supply, the displacement of thousands of residents continues, which in turn suppresses property values and slows community recovery.

The Consumer Insurance Crisis

The January 2025 Los Angeles wildfires severely impacted California’s fragile homeowners’ insurance market. They led to accelerated insurer withdrawals, premium increases, and thousands of policyholders being underinsured or without sufficient coverage.

The Southern California wildfires (the costliest wildfire event in world history, causing around $40 billion in insured losses and more than $53.8 billion in total economic damage) left an uninsured gap of over $13 billion.

Private Insurer Reluctance

Even prior to the 2025 fires, insurers had already begun to retreat from California’s highest-risk markets.

- State Farm stopped accepting new California homeowner policies in 2023 and withdrew 72,000 residential policies.

- Allstate, Farmers, The Hartford, and USAA also suspended homeowner coverage in specific high-risk areas.

- Other insurers gained regulatory approval to impose premium increases as wildfires worsened.

California’s Sustainable Insurance Strategy

As many insurers reduced their coverage, California’s FAIR Plan rapidly expanded, growing to around 668,000 policies by the end of 2025, four times its previous size.

From October 15, 2026, FAIR Plan premiums will (on average) increase by around 29%: while some homeowners will receive reductions, others face increases of over 50%, depending on the risk of wildfires and the property type.

Despite ongoing market instability, California’s average homeowners’ insurance premium remains comparatively low at about $1,600 a year, a figure that puts it well below the national average and substantially less than other states facing similar catastrophe risks, such as Texas ($4,085), Louisiana ($5,986), and Florida ($7,136).

Continuing Impact on Survivors

As of April 2026, as well as many former Pacific Palisades and Altadena residents remaining displaced, insurance benefit issues represent an additional source of hardship.

- 38% of survivors have already used their temporary housing coverage.

- 22% are now without any displacement benefits.

- Only 16% have over a year of housing coverage left.

Many families lack the financial resources to make up the difference once insurance benefits run out. Among households earning less than $50,000 a year, under one-quarter believe they could afford the costs of replacement housing for over three months without insurance assistance.

Claims Challenges

Many policyholders continue to suffer insurance claim delays and disputes. 40% still have open claims that involve dwelling damage, personal property, or temporary housing, while others say their claims have been denied or disputed. Homeowners with some structural or smoke damage suffer significantly higher denial rates than those whose homes were lost.

The most frequently cited problems include the following.

- Extensive personal property inventory demands (80%)

- Communication lags with adjusters (two-thirds)

- Multiple adjuster reassignments (40%)

- Coverage reductions and disputes regarding testing, remediation, or repair costs (50%)

Fewer than 10% of policyholders believe insurance claim conditions are improving.

Ultimately, wildfire losses increasingly extend beyond the fire, affecting housing availability, lending, insurance rates, and long-term community recovery.

Rebuilding Costs

Although 72% of survivors plan to rebuild or repair their homes, affordability is the main obstacle.

Homeowners estimate that they need an average of over $600,000 beyond expected insurance proceeds to fully rebuild their home. Displaced renters estimate that they’ll need around $250,000 to replace lost personal property and secure long-term housing.

‘Inadequate’ Government Assistance

More than a year after the 2025 Los Angeles wildfires, many survivors continue to suggest that limited government help has led to prolonged financial hardship, as well as uncertainty about their long-term recovery.

Satisfaction with the federal response to wildfires remains low. Only 17% of survivors report being satisfied (59% are dissatisfied, with 44% very dissatisfied).

Most survivors received very little help beyond FEMA’s initial $770 emergency payment.

- 59% got no additional FEMA aid.

- Only 14% received further FEMA help during the past year.

- 64% received no disaster loan help from the Small Business Administration (SBA), while just 21% received SBA disaster loan funding.

Crucial Community Support

Community organizations have consistently outperformed government agencies when it comes to helping survivors.

- 48% of survivors were satisfied with local nonprofits and faith-based organizations.

- 34% were satisfied with national charitable organizations.

- 50% received help from community organizations, while 60% received aid from philanthropic groups like the Red Cross and FireAid.

Despite community help to plug sizable gaps, the largest group of survivors (41%) describes themselves as hopeful but uncertain, with many uncertain as to whether long-term recovery is financially feasible.

California’s Recovery Measures

To help, California has implemented several emergency measures designed to facilitate faster rebuilding and reduce financial hardship.

- The suspension of permit requirements under parts of the California Environmental Quality Act and California Coastal Act to hasten rebuilding projects.

- The extension of tax filing deadlines, delayed property tax penalties, and expanded mortgage relief for affected homeowners.

- A $125 million mortgage relief program for wildfire survivors.

- The temporary suspension of new building code mandates for reconstruction projects.

- The expansion of protections to curtail price gouging for housing, hotels, construction materials, and other key goods.

- The provision of emergency support to help displaced students return to school and to help fire-affected school districts recover.

Ultimately, the initiatives have fallen short: survey data tells us that many survivors continue to face significant financial, housing, and recovery challenges.

The disparity between community support and government assistance emphasizes the long-term economic impact of wildfires and the ongoing need for sustained, actionable recovery strategies.

American Wildfires: Increasingly Dangerous, Complex, and Costly

Wildfires in the United States have evolved from seasonal natural disasters into year-round crises driven by climate change, human activity, infrastructure failures, and growing economic and insurance challenges. According to the Western Fire Chiefs Association, wildfires now burn nearly twice as many trees as they did in 2004.

The January 2025 Los Angeles wildfires (including the Palisades and Eaton Fires) became the costliest wildfire event in history. It killed 31 people, destroyed more than 16,000 buildings/structures, displaced around 100,000 residents, and caused economic turmoil with losses estimated between $76 billion and $131 billion, and insurance losses coming in at $40-45 billion.

Investigators allege that the Palisades Fire was a reignited ‘zombie fire,’ highlighting the rising threat such dormant fires represent.

Zombie fires continue to smolder in peat, roots or organic soils before reigniting months (or even years) later when conditions become more fire–favorable

The disaster exposed long-term permutations beyond fire devastation. Property values in the Pacific Palisades and Altadena areas fell by around $8.3 billion. Rebuilding is slow, and thousands of residents are still displaced.

Concurrently, California’s insurance market was subject to a significant downturn as major insurers reduced their coverage, FAIR Plan enrollment surged, premiums increased, and many policyholders faced delayed or disputed claims alongside often unfeasible rebuilding costs.

Survey data also confirmed broad dissatisfaction with government disaster help, with nonprofit organizations and community groups emerging as vital sources of recovery support. Although California has introduced some measures to help with rebuilding and the expansion of financial relief, wildfire risk continues to spread and intensify across the country.

Clearly, rebuilding or repairing homes is getting more difficult. Out-of-pocket cost is now the single greatest barrier to rebuilding (and is a factor cited by nearly 2 in 5 survivors).

For most Americans, insurance simply doesn’t cover the full cost of a rebuild: the median gap between insurance payouts and rebuilding costs is now at $500,000-$600,000 for homeowners. Additionally, nearly 1 in 3 renters report needing more than $200,000 to recover their losses.

Overall, the findings in this study confirm that modern wildfires are no longer isolated environmental events but complex social, economic, legal, and public policy challenges that demand sustained investment in fire prevention, fire resilience, insurance reform, and long-term recovery.

And it’s also clear that an inability to purchase homeowner insurance is one of the key issues stifling the recovery of California’s housing market. Without the necessary solutions, such as affordable, effective insurance and a better fire-combat strategy, the crisis will quickly worsen.

California wildfires destroy countless structures and impact countless lives every year. Many home and business owners take months or even years to recover their losses. If you have suffered losses from the devastation caused by a wildfire, you may be able to seek compensation for your damages.

California’s compassionate wildfire lawyer will pursue insurance claims, work with insurers, and file lawsuits to pursue available compensation under applicable law. (Sweet James Accident Attorneys focus on personal injury matters: call today for a free, no-obligation consultation and learn how our personal injury lawyers can help.)

Call or text (800) 900-0000 or complete a Free Case Evaluation form